A home loan in India is one of the most convenient revenue sources for home buyers. When an applicant or individual applies for a home loan, they generally undergo a stringent documentation and approval procedure. As loan amount for home loans is massively huge, lenders follow a rigorous process for determining the applicant’s eligibility. Moreover, HDFC home loan interest rates, SBI home loan interest rates and interest rates of other lenders are even decided after strict scrutiny of the home loan applicant’s application.

Note that large home loan amounts clubbed with long repayment tenures of the home loan need long term commitment from the borrowers. Any incorrect decision or faulty choice by the borrower can decrease their chances of getting their home loan approved and even adversely impact their future repayment capacity.

Thus, as a home loan applicant, you should know that the home loan repayment process holds the chance of draining you financially if you are not regular with your home loan EMIs. And also, the interest amount of the home loan furthermore adds to your woes. However, if you hold a definite approach, repayment should not be a hassle for you. Here, first, we will discuss basic tips you should consider when availing of home loans and then we move on to home loan repayment tips.

Basic tips to factor in when taking up a home loan:

Accumulate sufficient corpus for meeting your home loan down payment/margin contribution

Lenders through a home loan are allowed to finance up to 75-90% of the property’s value as per RBI guidelines. Depending on the lender’s credit risk evaluation of home applicants, the final proportion is decided. The remaining amount requires to be contributed by the applicant’s own resources. This implies, applicants before submitting their home loan application, should first aim at accumulating at least 10-25% of the property’s value. Failure to do so may result in loan application rejection.

Those home loan applicants looking to lower their interest costs should contribute a higher amount from their own resources. Higher contribution even enhances their chance of availing of home loan approval because it lowers the lender’s credit risk. While you do so, avoid compromising your emergency fund and investments especially allocated towards your crucial financial goals, to make higher contributions. In events of immediate financial emergencies or requirements to meet crucial financial goals, the absence of their respective funds unnecessarily may force you to avail of loans at higher interest costs.

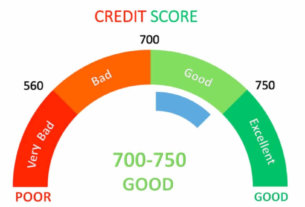

Go through your credit report before submitting the home loan application

A credit score is an important parameter factored in by lenders when evaluating the home applicant’s creditworthiness. Applicants who want to avail a home loan with a good credit score of 750 and above are most preferred by lenders as they are considered more financially disciplined and thus have reduced credit risk. These home loan applicants even have higher chances of home loan approval and are even offered lower HDFC Home Loan Interest rates, SBI Home Loan Interest Rates or lower interest rates by other home loan lenders because of their higher scores.

Thus, those applicants planning to apply for a home loan should ensure to fetch their credit reports. Doing so would enable those with lower credit scores to take the required measures to improve their score before submitting their home loan application.

Compare home loans offers from multiple lenders

Basic parameters such as processing fees, rate of interest, loan tenure, LTV ratio, loan amount provided by lenders usually widely vary based on the applicant’s credit risk assessment. Thus the applicants, before submitting their final application, should compare home loan offers from numerous lenders.

Applicants should initially start their search for a home loan by approaching financial institutions with whom they already have an existing relationship. Next, they should approach online lending markets for comparing home loan offers offered by other lenders. The final home loan application must be with the one offering the lowest rate for optimal loan tenure and loan amount.

Examine your EMI affordability

Home loan lenders consider the repayment capacity of the applicant while assessing their application. Usually, lenders prefer applicants’ EMI, including their new home loan EMI and other existing loan EMIs, if any, to be within 50-60% of the GMI (Gross Monthly Income) or NMI (Net Monthly Income). Those applicants surpassing this set limit have reduced chances of getting their home loan application approved.

For enhancing your home loan approval prospects, applicants must consider keeping their loan repayment obligations under 50-60% of their GMI or NMI. This can be done either by lowering their existing loan EMIs by foreclosing or prepaying some of their existing debts or by opting for longer repayment tenures or higher contribution from own funds (down payment) to new home loans for lowering their total EMI outgo.

Also, remember that the EMI of any loan is set on the basis of rate of interest, loan tenure and loan amount. While lower EMI results in higher tenure and higher interest cost, higher EMI results in shorter repayment tenure and lower interest cost. Thus, home loan applicants should take the help of online home loan EMI calculators to know their optimum EMI on the basis of their repayment capacity.

To know their optimum EMI, applicants should even factor in their mandatory monthly expenses, monthly contribution towards their financial goals, insurance premiums etc. Applying for a home loan after knowing your optimum EMI can lower your chances of defaulting on EMI owing to unplanned aggressive repayment schedules.

Basic home loan repayment tips

Loan prepayment: One can lower their HDFC Home Loan Interest rates, SBI Home Loan Interest Rates or interest rates of other lenders by prepaying the outstanding home loan amount. However, you must confirm one thing with the home loan lender before opting for this route, i.e. if there are any charges attached to prepayment. Few lenders offering home loans at fixed rates charge prepayment charges on their prepayments. In case your home loan is based on a floating interest rate, there will be zero imposition of any pre-closure charges.

Do not opt for longer repayment tenure: Longer repayment tenure for home loans equates to a higher interest component. In place, select shorter repayment tenures if you are financially stable. It would ensure that your home loan repayment process gets done faster at a much lower interest component outgo.

Enhance your home loan EMI: In case you are financially sound, then choose to enhance your home loan EMI by 5 per cent every month or prepay surplus amount in a year. By doing so, your interest component outgo would fall by a great extent. However, before you choose this route, ensure to estimate your monthly financial requirement to calculate the additional home loan EMI amount that you can afford in case of salary increment or on receiving an annual bonus.